Final market sustainability plan

Section 1: Revised assessment of the current sustainability of local care markets

Assessment of current sustainability of the 65+ care home market

As of March 2023, 334 Lancashire care homes are registered to support residents aged 65+ offering 11,800 registered beds. Of these 232 homes are residential and 102 offer nursing care. Lancashire County Council (LCC) currently fund approximately 4,200 long term residential and nursing placements.

Lancashire currently has a sufficient supply of residential and nursing home beds to meet demand with an overall vacancy level of 10%. However, there are some challenges with less availability in the North of the County. The care home population however is increasing to pre-pandemic levels and it is likely that further beds will be required in the next 5-10 years particularly catering to those people with dementia. We are currently analysing our future projected needs in order to share this with the residential and nursing care market.

There are already trends emerging of increased demand for specialised care, such as nursing care and dementia care (including those with behaviours that challenge) and a reduction in demand for standard residential care. Projections are for these trends to continue. This is a result of the increase in the older population expected to be residing in the county and people’s needs becoming more complex as they age.

A large percentage of Lancashire homes are relatively small and run by local care providers. The average residential home is 28 beds. Nursing homes tend to be larger with the average home being 52 beds. This relatively large percentage of small, independently run care homes may suggest that there is room to increase the number of larger homes in Lancashire where the investment in new facilities can be linked to a more sustainable financial position due to increased revenue overall.

The care home market is characterised by around 20% self-funders with around 4,200 long term care home beds (36%), commissioned by the local authority. Approximately 16% are joint funded and circa 20% funded by health partners, some of which are block booked for Discharge to Assess or system resilience.

Care homes are commissioned by the Council on a spot purchase basis and a contract is offered to any CQC registered provider that will accept the local authority fee rates. This allows for any new entrants to the market to develop a relationship with the local authority immediately on starting up in Lancashire. Regular communication and engagement with providers is carried out through a specific quarterly forum that looks to share market information between commissioners and providers. Additionally, specific engagement takes place with all providers each year to set fee levels.

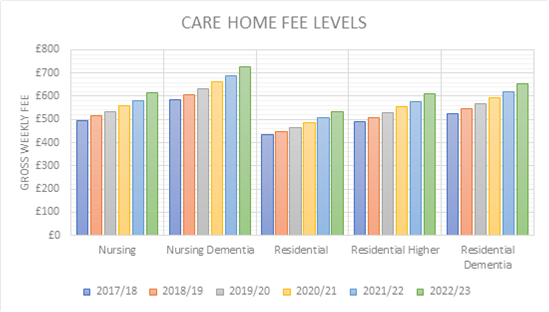

The graph below shows the trend in average fee rates since 2019/20

Like other local authority areas, care homes in Lancashire were adversely impacted by the Covid 19 pandemic with, at times, up to two fifths of care homes closed to admissions due to a Covid 19 outbreak. Additionally, we experienced low overall occupancy levels particularly in the residential care only market.

As with other sectors, care homes have struggled with recruitment and retention of care staff, nursing staff and ancillary workers such as cleaners resulting in a substantial increase in the use of more costly agency workers which can affect the quality of care delivered since agency workers are less familiar with the needs of residents and the policies and procedures in the home. Evidence gathered via administration of COVID support grants indicates providers were charged in excess of £50 per hour for agency staff. Other impacts on the market are as follows:

- An impact on staffing levels and retention of staff

- Some homes with lower occupancy levels, particularly residential only settings

- An overall increase in demand for elderly mental health placements in residential care and nursing care

- Financial viability of residential care with a number of home closures amongst smaller residential homes

- Challenges with the Discharge to Assess (D2A) scheme

Inflationary pressures continue to impact on the residential care home market particularly in relation to high energy costs and this is despite government support in this area. National Living wage increases are higher than expected too from April 2023. Lancashire County Council have utilised its Fair Cost of Care funding to increase care home fees between 16%-20% from April 2023 to ameliorate the impact on the care home market.

Delays to Charging Reform have not impacted on our approach to increasing fees for 2023/24 however it is still recognised that there remains a difference between the local authority rates and those fees paid by self funders.

Assessment of current sustainability of the 18+ domiciliary care market

Lancashire County Council currently commissions approximately 88,000 hours of homecare services per week. The current homecare contract commenced in 2017 as a provider framework and is due for renewal in 2023. We reduced the number of providers, who all now work on an area basis to make the service more cost effective by reducing travel time. The framework was designed to address supply issues in some parts of the county and deliver a more sustainable market characterised by more meaningful choice.

Homecare framework providers have a range of hourly rates which were initially set at the commencement of the framework however there is a clause in the contract which allows a provider to request a price review under certain circumstances and some providers have requested this and been awarded a higher rate. Through benchmarking with other local authorities in the region, we are aware that our average fee rate is currently among the highest in the North West.

Despite initial success through the introduction of the framework, we have increasingly had to commission services “off framework” where average fee rates are almost 20% higher, to meet demand pressures. 31% of commissioned hours are now 'off-framework'.

In reducing our reliance on residential care and increasing our ambition to help people to remain at home where possible, we will increasingly rely on homecare to meet needs. This will mean increasingly requiring specialist support from homecare providers for people living with dementia.

There are a number of gaps in provision which include difficulties in sourcing home care in the more rural North of Lancashire (Lancaster, Fylde and Wyre) and also periodically in some urban areas (Burnley, Chorley and South Ribble).

Fee rates have been increased year on year following engagement and cost exercises with providers. We have focused the use of the Market Sustainability funding on our homecare framework in 2022/23 to give an above inflationary rise in fees to assist with cost pressures, the recruitment and retention of staff and to try to ultimately reduce our reliance on non-framework provision.

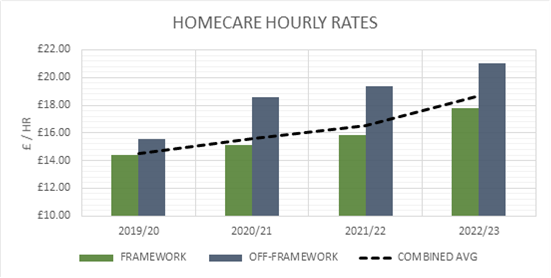

The graph below shows the trend in average fee rates since 2019.

Providers are currently struggling to recruit and retain a suitably skilled workforce due to a combination of competition from other sectors which pay more for less demanding work, cost of living increases particularly in petrol costs, a negative image of working in social care and the emotional demands caused by the pandemic.

Some providers have had to increase wages to stay competitive and although many providers pay above the National Minimum Wage they are having to increase wages across the board to compete with other providers in the area and with care home, supported living and extra-care providers who do not have the added burden of travel costs.

Providers are experiencing rapidly increasing cost pressures on other areas such as increases in NI contributions, food costs, energy costs, motor fuel costs, pension contributions, insurance costs and CQC registration fees. Providers report that the factors listed above have created an unsustainable business environment. Over the last 12 months, many have been actively increasing the percentage of self-funders they work with as they state they are making a loss for every hour they provide services for the council.

NHS partners have increasingly utilised home care provision to support discharge from hospital offering block contracts to providers. This has had the effect of increasing demand and driving up cost for the local authority as framework provision becomes more difficult to source.

The impacts of the current market pressures are as follows:

- Demand for home care has increased by over 15% from levels prior to the start of the pandemic. This is likely to be as a result of our stronger focus on 'care at home' and less reliance on residential care.

- Waiting lists for domiciliary care have increased. Prior to the pandemic in March 2020, approximately 10 people equivalent to 80 hours were awaiting a package of care. In November 2021, 197 people equivalent to 1,500 hours were awaiting a package of care and in September 2022, 140 people equivalent to 1,120 hours are currently awaiting a package of care.

- The number of people awaiting a double handling package of care has increased accordingly however the percentage of these double handling requirements against the overall number of people requiring a package of care is higher than previous, indicating that people with higher levels of need are requiring home care.

32 packages of care have been handed back to the Council in the last 3 months

Inflationary pressures continue to impact on the home care market and the outlook remains uncertain. National Living wage increases are higher than expected from April 2023. Lancashire County Council has utilised its Fair Cost of Care funding to increase home care fees for our framework providers by 12.62% from April 2023 to take into account the inflationary increases and work towards a fair cost of care. The majority of homecare providers however already pay their staff at real living wage rates or above based on the results of our Fair Cost of Care exercise.

Section 2: Assessment of the impact of future market changes between now and October 2025, for each of the service markets

Based on projections from the Projecting Older People Population Information System (POPPI) between now and October 2025, the number of people 65+ will increase by 4% with the 85 and over age group also increasing by 4%. This will likely result in a proportionate increase in people with long term health conditions.

This increase in the older population and the prevalence of mental health problems, physical disabilities and co-morbidities amongst older people will have a significant impact on demand for services, with initial projections suggesting an additional 1,000 people requiring support by October 2025.

The complexity of need has increased as a result of the Covid 19 pandemic as evidenced by the increase in double handled packages of care. This places a further strain on costs of delivery and recruitment and retention of sufficient care workers.

There is some evidence to suggest that demand for accommodation based services has reduced due to the challenges faced by care homes during the pandemic e.g. Covid outbreaks and visiting restrictions. If this continues it will impact on the financial sustainability of some homes due to vacant beds and put further strain on community based services due to increased demand.

Continuing uncertainty around inflation and particularly energy costs places considerable pressure on residential care homes to maintain their financial viability. It is possible that there will be some closures of smaller homes where it is more difficult to absorb the increased costs however we are also seeing a number of larger new homes opening.

Section 3: Plans for each market to address sustainability issues, including fee rate issues, where identified

Overall care market

It should be noted that the data collected from the Fair Cost of Care exercise raised many issues around the validity of it's use in determining a 'Fair Cost of Care' which we have illustrated in our Annex B submission to DHSC. However, not withstanding our concerns, we have given due regard to the information we have received along with our assessment of market pressures and direction of travel in determining use of the Fair Cost of Care funding.

We are transforming our practice through our 'Living Better Lives in Lancashire' (LBLiL) transformation program. Our vision is that together, the people we serve, will have greater choice and control in living a good life, staying connected and engaged with communities and supported in their own homes for longer. At the heart of this is a strengths based approach to all of our work, to ensure people are connected to support that maximises their independence, utilises a persons individual and community based assets and formal care and support complements when required. This transformative approach will also help to address increasing demand across the whole care market in Lancashire.

65+ care homes market

Fair cost of care

The rates for the Fair Cost of Care as calculated via the DHSC prescribed methodology for each bed type are set out in the table below.

| Bed type | Placements at August 22 | Standard contract rates | Avg Fee Paid* | 22/23 Fair Cost of Care Adjusted |

|---|---|---|---|---|

| Nursing | 456 | £614 | £619 | £685 |

| Nursing Dementia | 376 | £726 | £722 | £709 |

| Residential | 544 | £535 | £547 | £672 |

| Residential Higher | 919 | £609 | £610 | £X* |

| Residential Dementia | 1,370 | £655 | £655 | £688 |

*The county council operates 5 fee levels across care home services. The DHSC exercise did not collate information relating to a Residential Higher fee level. Contract rates are show for context.

Plans to move towards the FCOC

The costs associated with uplifting 65+ care home placements to the fair cost of care as calculated during this exercise are unaffordable within the Council’s existing resources and do not necessarily represent a fair cost of care due to the issues raised in our Fair Cost of Care, Annex B submission. The Fair Cost of Care exercise did not take into consideration the cost of care for younger adults care homes and therefore this is a further cost pressure to be considered against future increases in fees.

2022/23

The Council has used the majority of its allocation of MSF (£3.7m) to support higher than inflation uplifts for home care fees and uplifts to all other market areas at inflation or above. In total, the council has invested significantly more than the MSF grant.

The county council uplifted homecare fees by over 13% in 22/23 representing over £4.5m additional spend. The Council also uplifted care home fees by 5.6% from April 2022 (approx. £10m additional spend). The total cost of fee uplifts in 2022/23 across the entire market with which we contract was approx. £25m (£8m in excess of Medium Term Financial Strategy estimates). Provider fee rates for care homes across Lancashire are among the highest in the North West as evidenced through benchmarking however the Council recognised the issues in recruitment and retention of staff being experienced by our providers and committed to maintain our strong fee rates to ensure a sustainable care market.

2023/24

The Council has continued to use the government grant monies (formerly Market Sustainability Funding) to uplift the standard contract rate for residential and nursing home placements by between 16% and 20%. The new rates would be applied to current placements from 3rd April 2023 that are at or below the new rates.

These higher than inflationary uplifts recognise the particular issues that care home operators are experiencing through increased energy costs and allow for the significant rise in national living wage rates from April 2023. We also encourage investment in new care homes and the refurbishment of existing ones by offering more attractive fee rates to providers wishing to operate in Lancashire.

We will also continue to work closely with care home operators in Lancashire through our provider led forum, sharing opportunities and data to inform the market and receive feedback from them to develop future provision in line with the needs laid out in our recently refreshed Market Position Statement.

2024/25

The Council plans to use Market Sustainability Funding to maintain the standard contract rates for 2023/24. This assumes FCoC and MS Funding equivalent to that received in 2023/24.

18+ domiciliary care market

Fair Cost of Care

Data provided by homecare providers appears to be more consistent and raises less concerns about validity of information provided. The council conducted a fair cost of care exercise in 2021 and rates are consistent for both exercises.

The impact of uplifting rates for domiciliary care to the Fair Cost of Care rate has implications for other types of care which sit outside the scope of the Market Sustainability Plan such as Direct Payments, Complex Care, Supported Living and Rapid Response, Reablement, Crisis support and Extra Care as many providers of homecare also deliver care in these services and may not accept a different hourly rate.

The Council will need to consider conducting similar cost exercises for these services to determine fair fee rates and avoid unintended consequences including an impact on recruitment and retention of staff in other adult social care provider market areas.

2022/23

The Council has used the majority of its allocation of MSF (£3.7m) to support higher than inflation uplifts for home care fees and uplifts to all other market areas at inflation or above. In total, the council has invested significantly more than the MSF grant.

The county council uplifted homecare fees by over 13% in 22/23 representing over £4.5m additional spend. The Council also uplifted care home fees by 5.6% from April 2022 (approx. £10m additional spend). The total cost of fee uplifts in 2022/23 across the entire market with which we contract was approx. £25m (£8m in excess of Medium Term Financial Strategy estimates). Home Care provider fee rates in 2022/23 in Lancashire are among the highest among North West authorities currently.

2023/24

The Council has continued to use the government grant monies (formerly Market Sustainability Funding) to uplift the standard contract rate for our 'framework' home care provision by 12.62% which broadly brings the average fee rate in line with the results of our Fair Cost of Care exercise. The new rates would be applied to current packages of care from 3rd April 2023.

These higher than inflationary uplifts recognise the particular issues that home care providers are experiencing in terms of difficulty in recruitment and retention of staff and allow for the significant rise in national living wage rates from April 2023. However, our fair cost of care exercise revealed that the majority of home care providers are already paying staff hourly rates at or above the Real Living Wage.

Our new contracts for homecare will commence from November 2023 at fixed rates which will be set above the current average framework fee rates to encourage more providers to work with Lancashire under its contractual framework and increase quality and sustainability of provision. Further enhancement to rates will be made where additional travel time is required in some of our more rural areas for example.

We will also continue to work closely with home care providers in Lancashire through our provider led forum, sharing opportunities and data to inform the market and receive feedback from them to develop future provision in line with the needs laid out in our recently refreshed Market Position Statement.

2024/25

The Council plans to use Market Sustainability Funding to maintain the standard contract rates for 2023/24. This assumes FCoC and MS Funding equivalent to that received in 2023/24.

The Council has worked closely with home care providers to understand some of the key barriers to sustainability and has utilised the information received to develop our strategy in commissioning homecare over the next 10-12 years. The Council is now in the final stages of re-tendering its home care services and will aim to address some of the issues around recruitment and retention detailed previously through consideration of fixed rate fees, supplements for areas where care hours are more difficult to source, consideration to block contracts in some circumstances and a focus on working with our health partners and providers to address the overall supply and demand issues.